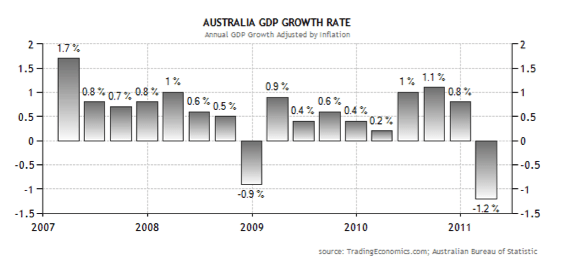

Australia’s recent GDP figures triggered an additional downwards shift in the markets. Although it was highly anticipated that the aftermath of the QLD floods and the Japanese tsunami had a dramatic impact on Exports, investors were shocked by the -1.2% figure for the 1st quarter of 2011.

This was the first negative result since the 4th quarter 2008, which in the height of the GFC (Global Financial Crisis), had posted a -0.9% growth rate.

GDP, or Gross Domestic Product, measures the market value of a basket of goods and services produced within a country. As different countries produce different goods and services, there are variations to what is included in the GDP calculations.

For a country to grow and prosper, it needs to maintain a steady GDP growth rate. The ideal GDP growth rate is one that is sustainable and maintains an economy in an expansion phase of the business cycle. Between 2 to 3% annual growth is considered to be ideal while consistent figures above 4% would be considered too high, and negative figures define a shrinking economy.

Too high a growth rate will result in the economy growing too fast, and applying pressures on Inflation and Interest Rates. This usually creates an Asset Bubble of some type, just like the Technology bubble of 2000, and the Housing bubble of 2008. Technically speaking, two consecutive quarters of negative GDP growth defines a Recession.

When economies are expanding, the general price of goods and services rise. This is referred to as Inflation. If Inflation is increasing too significantly, it puts pressures on the cost of living. Central Banks will then raise Interest Rates in an attempt to slow Inflation down.

What we are experiencing at the moment is a very rare situation. We have negative GDP growth, however, the cost of living and inflation is actually expanding. This rare situation is commonly referred to as Stagflation.

So we have this situation where the cost of living is increasing, but there is negative economic growth. If Interest Rates are raised to slow the economy down, it could actually worsen GDP growth and in turn Unemployment would increase and the economy would grind to a halt.

Alternatively, leaving Interest Rates alone to help instigate economic growth would result in the cost of living continuing to increase. Consumers would be priced out of the economy and spending would decrease. Less spending results in a slowing economy and subsequently an increase in Unemployment. Again, a negative for the economy.

So in a state of Stagflation, there is virtually no positive outcome. Hence governments and central banks attempt to avoid these situations. The last, most predominant period when Stagflation affected the economy was during the oil crisis of the 1970’s.

Recently, you may have heard the terminology “2-Speed economy”. It’s a relatively new term that simply describes the difference between the Haves and Have-nots. On one hand we have the “Mining Boom” where all involved are experiencing great wealth as demand for our natural resources is helping feed the China boom. On the other hand, nearly all other sectors are showing weak or negative growth.

Both QLD and WA are said to be reaping in the benefits of the Mining Boom, whereas the rest of the country is experiencing higher costs of living, stagnant wage growth and slumping property values.

Statistics show that Australia has actually been in this “2-Speed” economy for some time. The populations in QLD and WA have been growing long before the mining boom, and reality is that many of the high wage miners are “Fly-in, Fly-out”. Which means they earn the big dollars out at the mines, and take the money home interstate.

The real disparity has occurred for 2 reasons:

1) The real wealth in Sydney and Melbourne had come from growth in property values, and

2) The Australian economy is dominated by its services sector, but our economic success is based on mineral resources and agriculture.

As we can see from the following data, the Services sector represents the greatest percentage of GDP, however, Minerals are our largest export by value. This is mostly due to the fact that we have a small domestic market and there is high global demand for our minerals and agriculture.

|

Sector |

% of GDP |

Exports $M (2010) |

|

Services |

71.3% |

52,391 |

|

Industry |

24.9% |

69,491 (Minerals) |

|

Agriculture |

3.8% |

30,326 |

This offers us great insight into what we should be doing in these current market conditions.

Growth for the coming 6 to 12 months will be in the Resources/Mining sector. Demand is expected to remain strong for our natural resources despite China slowing and Australia operating in a 2-speed economy.

The Services sector will be an anchor to the Australian economy. Consumer spending has decreased and savings rates have increased. The Property market remains weak and investor confidence is overwhelmed by the negativity from “sovereign debt” issues flowing from around the world. Subsequently, this will put pressure on the value of related stocks.

Our focus has been to establish investment positions in Resource stocks, with minor portfolio exposure in other industries. During the recent market downturn (May/June 2011), this has helped maintain a minimal value loss to our portfolio. We have also been able to profit during this market correction by using Protection strategies using the S&P ASX200 index.